- Analytics

- News and Tools

- Market News

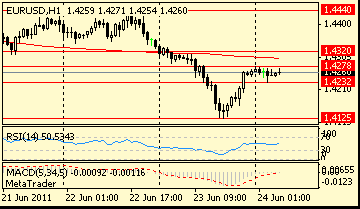

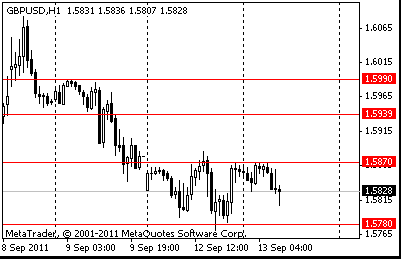

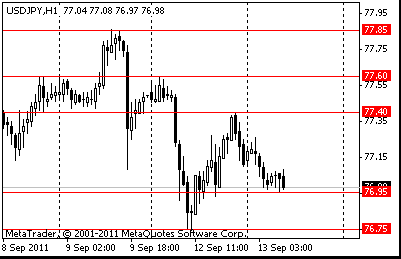

- Forex: Monday's review

Forex: Monday's review

IEA monthly oil market report is due, at 0800GMT.

UK data at 0830GMT includes inflation and trade data as well as CLG House Prices. Consumer Price Inflation is expected to show price increases persisting at well over double the 2% official target. The BoE has said it expects CPI to approach a 5% annual rate once rising utility bills take their toll but that is not expected to be seen until the September data are released next month. Median forecasts for Tuesday look for CPI to come in at 0.6% m/m, 4.5% y/y with core-CPI at 0.6% m/m, 3.1% y/y. Trade is due out the same day and could well reflect the clear drop off in demand and orders from overseas seen in the recent Markit/CIPS PMI survey of the sector.

US data starts at 1230GMT with the Import/Export Price Index. Increases in import prices may be moderate due to only a small change in petroleum costs, and smaller increases in items like foods and motor vehicles. Export prices should benefit from favorable exchange rates and demand for agricultural products.The two earliest monthly indexes for consumer confidence include the IBD/TIPP Economic Optimism Index for September at 1400GMT and could provide a strong hint about the direction of the preliminary Reuters/University of Michigan Consumer Sentiment Index on Friday. Finally, at 1800GMT, the US Treasury is expected to post a $130.0 bn budget gap in August.

© 2000-2026. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers